The Rule of 72

After a strong recovery in markets since the COVID setback, we’re finding a lot of people are anchoring around double their money lately. This is an area we can add value—not to promise quick riches, of course, but to highlight the Rule of 72.

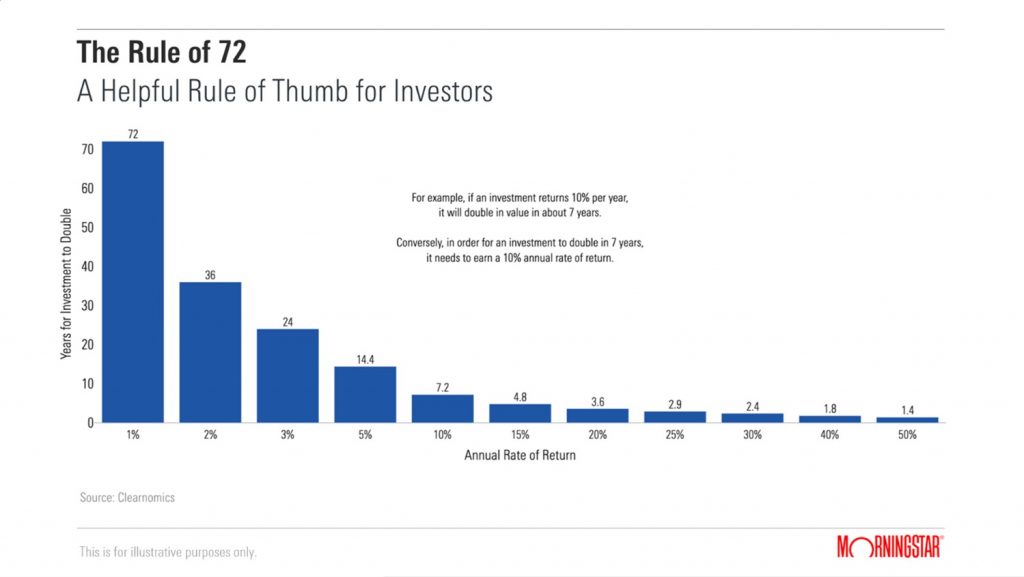

The ‘Rule of 72’ tells us how long it will take to double our money in the markets, conversely it demonstrates how much we miss out on by leaving our money in cash. It supports the old adage that investments in growth assets tend to double approximately every 7-10 years (such as shares or property), while investments in defensive assets might take 15-35 years to double in value (such as bonds).

Used correctly, the Rule of 72 can be an important factor that we must weigh up when we invest, or rather don’t invest. It works for young clients who want ultra-fast returns, helping to base expectations on reality, but also older generations who may feel tempted to park in cash.

What is the Rule of 72?

Simply put, it tells us how long it will take us to double our money, at different rates of return. It is a simple mathematic equation: Number of Years = 72 / Expected Return. If we expect to generate a 1% return each year, it will take us 72 years to double our money. If we expect to generate a 10% return, it’ll take 7.2 years. Looking at it in a different way, if we need to double our money in 10 years, we need to achieve a 7.2% return each year.

Of course, it just a rule of thumb, as markets don’t move in straight lines and forecasting future returns is incredibly difficult. But we know through research and experience, that there is a trade-off between risk and return. Taking more risk can lead to more return, but we should never take more risk than we’re comfortable with. This applies at all stages of life, but in slightly different ways:

•For Younger Generations

this rule showcases the power of creating good money habits, putting money aside to generate returns that compound each year, turning financial dreams into financial goals.

•For Older Generations

this rule is also very useful, but for different reasons. In this case, it helps illuminate the trade-off between safety and ambition—or risk and return. For most clients nearing retirement, we see a tendency for them to become more conservative, which is sensible in many respects, but they often forget they still have 30+ years of investing left in their lifetime. Sometimes, they still need to double their money to reach their retirement goals, but they fail to take enough risk to get there.

Even the Financial Conduct Authority (the body that regulates the financial services industry) came out with some interesting research that 8.6 million UK consumers have more than £10,000 of investable assets sitting in cash, despite having a higher risk tolerance. As the Rule of 72 would attest, holding too much cash might be detrimental to your long-term plans.

Final Thoughts

If you’d like us to explore the Rule of 72 and how it might apply to your investments, we would be happy to discuss this with you face to face or in a Zoom meeting or phone call. Our existing clients can take comfort from knowing their portfolio is invested in a diverse mix of assets and is designed to deal with a range of market forces and scenarios. If we get this right consistently enough, even accepting the odd speed bump, we’ll be well on our way to helping our clients get the most out of the Rule of 72.

Email info@brookswealth.co.uk. or call 01733 314553

Source of FCA research: https://www.fca.org.uk/publications/corporate-documents/consumer-investments-strategy.